For most of the twentieth century, retiring Americans could count on a simple arrangement: work long enough for a company, and receive a steady monthly check for the rest of your life. That was the pension era. It is largely gone now, replaced by 401(k) plans that hand the saving, investing, and spending decisions squarely to the individual worker. The results have been uneven. Today, however, something interesting is happening. The 401(k), long criticized for what it lacks, is being redesigned from the inside out to deliver something closer to what a pension once promised: income you cannot outlive.

The Collapse of the Traditional Pension and What Replaced It

The shift from pensions to 401(k)s is one of the most consequential changes in American financial life over the past five decades. One of the notable trends in the U.S. retirement system over the past five decades is that private sector employees have become less likely to be covered by defined benefit pension plans and more likely to be covered by defined contribution pension plans. The numbers tell a stark story. In March 2024, just 15 percent of private industry workers had access to a defined benefit plan – the kind that provides guaranteed retirement benefits based on plan formulas. That is a dramatic drop from the six in ten workers who had access to one back in the 1980s.

In 2023, DC plans had 93.4 million participants, while DB plans had just 11.1 million participants in the private sector. The 401(k) became the dominant vehicle almost by default, not necessarily by design. Though 401(k)s took off in the early 1980s, Congress did not intend for them to replace traditional pensions as the primary retirement vehicle, and 401(k)s are poorly designed for this role. That design gap is now the central problem the retirement industry is trying to solve.

The Core Problem: Saving Is Not the Same as Income

DC plans do not provide guaranteed income. The funds in the account experience investment gains and losses, and the contributions and earnings are used as a source of income in retirement. This puts the entire burden of managing longevity risk on the individual. Someone who retires at 65 and lives to 92 is drawing down a fixed pool of money – and the math is genuinely hard to get right without professional guidance.

As more Americans live longer, nearly two-thirds of workers saving for retirement worry they’ll outlive their retirement savings, according to BlackRock’s annual Read on Retirement survey, and 99% of those workers say having guaranteed retirement income would help. Social Security provides a foundation, but it was never designed to be sufficient on its own. Social Security payment guarantees were never designed to be the primary source of retirement lifetime income. In a perfect world, Social Security should be used as a secondary strategy. The gap between what workers need and what their 401(k) balance can realistically provide is what has pushed the industry toward a new model.

The SECURE Act and SECURE 2.0: The Legislation That Changed Everything

When the SECURE Act passed in December 2019, it fundamentally altered how employers could approach in-plan annuities. Among its most significant provisions was the establishment of a fiduciary safe harbor for selecting annuity providers, which significantly reduced employers’ liability concerns when incorporating lifetime income options. Before this, many plan sponsors simply avoided annuities altogether because the legal exposure was too uncertain. The safe harbor changed that calculation.

The SECURE Act and SECURE 2.0 significantly changed rules for in-plan annuities within 401(k)s. Employers now have a “safe harbor” for offering in-plan annuities, reducing their financial liability, while employees gain more access to lifetime income options and increased portability of annuity investments. Increased transparency and disclosure requirements also aim to help employees make informed decisions. As of 2025, the legislation requires businesses adopting new 401(k) and 403(b) plans to automatically enroll eligible employees, starting at a contribution rate of at least 3 percent. Auto-enrollment, combined with clearer income disclosures, is steadily nudging millions of workers toward more retirement-ready behavior.

Lifetime Income Disclosures: Seeing the Monthly Number

The SECURE Act created a new participant disclosure requirement for 401(k) plans. To meet this new requirement, benefit statements must include a “lifetime income” disclosure at least annually, to help plan participants understand how much income their current account balance could produce in retirement. That single change has more practical impact than many people realize. Seeing a projected monthly income number – rather than a raw balance – fundamentally reframes how workers think about their savings.

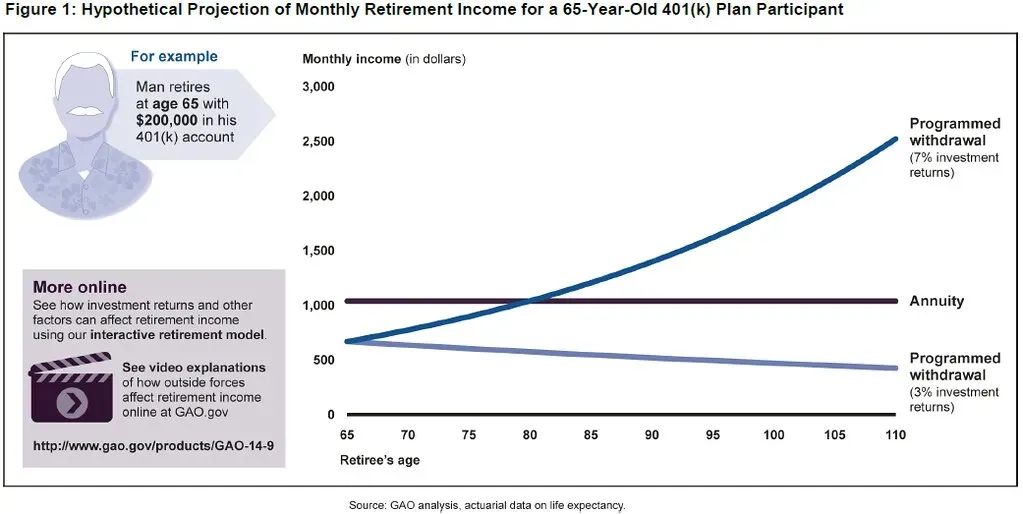

In practice, 401(k) participants tend to underestimate the savings they will need to sustain their desired level of income in retirement. For example, $100,000 can seem like ample savings until you realize it would only pay a 65-year-old about $500 to $600 per month in lifetime income. The disclosure requirement forces that reality to surface before it is too late. Plan sponsors must now provide annual statements showing how individual participants’ account balances would translate into monthly income in retirement. It is a quiet but meaningful shift in how the whole system communicates with the people it is supposed to serve.

Annuities Inside the 401(k): From Fringe Option to Mainstream Feature

Annuities are financial products that, at their most basic, turn an initial lump-sum investment into a guaranteed monthly payment that continues until you die, creating an income stream that you cannot outlive. An in-plan annuity allows you to convert some or all of your 401(k) into steady income, taking the guesswork out of timing withdrawals. For decades, annuities inside workplace plans were rare and viewed with suspicion. That is changing, though the shift is still in its early stages. The 68th Annual 401(k) Survey by the Plan Sponsor Council of America, published in late 2025, found that only 8.9 percent of respondents had an in-plan annuity for the 2024 plan year.

LIMRA research shows there has been a meaningful increase in workers’ willingness to convert assets into lifetime-guaranteed income, rising from 38 percent in 2017 to 52 percent in 2023. Employer interest is also climbing. A survey found that almost half of plan sponsors that did not currently offer an in-plan annuity said they have considered adding one, and about three in four claimed they would make this decision within the next 12 months. The demand is real, even if the adoption curve is still gradual.

BlackRock, Vanguard, and TIAA: The Giants Making Their Move

BlackRock’s LifePath Paycheck, a target-date solution that combines retirement income, quickly grew to be one of the largest lifetime income target-date strategies in the defined contribution market. The strategy closed 2024 with $16 billion in assets under management across six employer retirement plans. LifePath Paycheck first launched in April 2024 and provides access to guaranteed income through a target-date fund, offering retirement income to participants as early as age 59½ by purchasing annuity contracts issued by Equitable and Brighthouse Financial. This hybrid approach – keeping investments intact while quietly building annuity assets alongside them – is proving genuinely popular.

Vanguard, the nation’s leading provider of target-date solutions, deepened its commitment to retirement innovation through a collaboration with TIAA, a pioneer in guaranteed lifetime income. This collaboration brought together two trusted names to deliver a retirement income solution designed to provide retirees access to a guaranteed income stream for life. Vanguard developed a new target-date collective investment trust series, Target Retirement Lifetime Income Trusts, that incorporates the TIAA Secure Income Account as the lifetime income annuity option. TIAA paid more than $5.9 billion in lifetime income to retired clients in 2024, underscoring the scale of what these guaranteed income systems can ultimately deliver.

Qualified Longevity Annuity Contracts: The Long-Game Tool

A Qualified Longevity Annuity Contract (QLAC) is a deferred income annuity bought with qualified retirement money that delays payments until later in life and can remove the premium from required minimum distribution calculations for earlier years. For 2025, the lifetime contribution cap for QLACs is $210,000. Think of it as retirement insurance against living very long. You invest a portion of your 401(k) now and start receiving guaranteed monthly payments beginning at a later age, typically in your mid to late seventies or early eighties.

SECURE Act 2.0 and later updates through 2025 adjusted QLAC contribution parameters and clarified eligible account treatment. These milestones shifted how advisors and retirees view longevity income and RMD timing, making QLACs a practical option for managing tax exposure and securing late-life guaranteed income. The prior 25-percent-of-income limit rule was eliminated, making QLACs more accessible and easier to invest in. The strategy works particularly well for people who want to ensure they will still have meaningful income in their eighties and nineties, even if their other assets run thin.

What Still Stands in the Way – and What Comes Next

The roughly $29 billion in annuity-enhanced target-date funds is still a tiny fraction of the more than $4 trillion invested in target-date strategies overall. Adoption is expected to remain slow because of the added complexity of annuities and the need for better education on how to use them effectively. Employer inertia is part of the story too. Despite strong demand, roughly seven in ten plan sponsors are waiting for income solutions to become more mainstream before adopting them, citing concerns around information, education, cost, and value.

Research shows that individual savers in defined contribution plans can achieve, on average, a roughly 22 percent increase in potential retirement spending when they embed guaranteed retirement income solutions into a target-date fund. That is not a trivial gain. As employees demand simpler and more secure retirement solutions, employers face increasing pressure to address financial stress and rising retirement delays. With regulatory clarity, strong participant demand, and ready-built infrastructure, lifetime income is rapidly becoming the next major evolution in plan design. The infrastructure is largely in place. The question now is how fast plan sponsors, workers, and the broader industry move to use it.

Conclusion: The Retirement System Is Catching Up to What Workers Actually Need

The 401(k) was always a savings tool, not an income tool. For forty years, that distinction was mostly ignored. Now, through a combination of legislation, competitive pressure from major asset managers, and a growing wave of workers who simply cannot afford to run out of money, the system is adapting. Annuities embedded in target-date funds, mandatory lifetime income disclosures, expanded QLAC limits, and fiduciary safe harbors are all pieces of the same underlying shift: making workplace retirement plans look and behave more like the pensions they replaced.

The transition will not happen overnight, and not every worker will benefit equally. But the direction is clear. Changes now include making annuities portable so account holders can transfer them from one retirement plan to another, eliminating restrictions on annual payment increases so that in-plan annuities can better keep pace with inflation, and enhancing liability protections for plan sponsors to encourage broader employer participation. For workers nearing retirement today, the options are meaningfully better than they were just five years ago. The 401(k) is not yet a pension – but it is learning to pay like one.

{kind=link}