Nobody mugged you. Nobody raised your taxes officially. Yet somehow, your money buys noticeably less than it did just a few years ago. That sinking feeling at the grocery checkout, the shock when your insurance renewal lands in your inbox, the quiet moment of math when you realize your streaming subscriptions now cost more than a dinner out – it all adds up. Faster than most people realize.

This is what some economists and consumer advocates are calling the “invisible tax.” It doesn’t show up on a government form. Nobody voted on it. It just quietly arrives, bill by bill, purchase by purchase. So what exactly is eating your wallet alive? Let’s dive in.

Groceries: Your Cart Costs More Than You Think

Here’s the thing most people don’t fully absorb when they hear “inflation is cooling”: the prices don’t actually go back down. They just stop rising quite as fast. Overall prices are up roughly a quarter since January 2020, based on CPI data – more than double the cumulative inflation seen in the five years before that. Your grocery cart is one of the clearest places to feel that.

From March 2020 to January 2024, grocery prices rose about 25%, which is why your cart still feels expensive even as monthly inflation cools. That cumulative damage is baked into every shelf price. It doesn’t reset.

Beef and veal prices alone jumped nearly 15% year-over-year through September 2025, and a recent survey found that roughly nine in ten American adults are stressed about the cost of groceries. Honestly, it’s hard to argue with that number when you’re standing at the meat counter.

A handful of everyday staples – especially coffee and beef – are still seeing double-digit annual increases, even as some categories are finally moving in the right direction. The headline inflation number tells you things are better. Your receipt tells a different story.

Streaming Services: The Bill That Keeps Climbing

Remember when streaming felt like the cheap alternative to cable? Those days are genuinely behind us. Netflix’s Standard plan rose 94% over 12 years as it climbed from $7.99 in 2011 to $15.49 in 2023, while the Premium plan jumped 92% in ten years from its introductory price to $22.99. That’s not a small price adjustment. That’s a near-doubling.

In October 2023, Netflix raised the price of the Basic plan from $9.99 to $11.99 per month and upped the Premium price from $19.99 to $22.99. Then, just over a year later, the hikes came again. Netflix’s Standard plan jumped from $15.49 to $17.99 per month in January 2025, the ad-supported tier rose from $6.99 to $7.99, and the Premium tier climbed from $22.99 to $24.99.

Netflix’s latest 2026 price increases represent an average 11% hike across the product suite. And it’s not just Netflix. YouTube TV increased the price of its base plan by $10 in December 2024 to $82.99 per month, Disney+ raised prices in October 2025, Hulu with ads climbed to $11.99, and HBO Max raised its standard plan to $18.49. When you add them all up, the streaming bundle can easily eclipse what cable used to cost.

Auto Insurance: The Stealth Bill Nobody Saw Coming

Auto insurance is, without question, one of the most dramatic and least-discussed cost explosions of recent years. It’s not a purchase you browse for fun. You pay it, wince, and move on. According to Bankrate’s 2025 True Cost of Auto Insurance report, the average cost of a full coverage policy went up $625 – over 30 percent – from January 2023 to January 2025.

Car insurance prices are expected to increase an average of 7.5% in 2025, which is actually a significant slowdown from the prior two years when rates rose an average of 16.5% in 2024 and 12% in 2023. Let that sink in. Even the “slowdown” is still an increase piled on top of those already elevated rates.

The average cost of full coverage car insurance reached $2,638 in 2025, with Americans spending roughly 3.4% of their median household income on car insurance alone. For context, that share of income going to auto insurance is a number that has grown steadily year after year. These price increases are driven by factors such as increased claims, frequent natural disasters, and changing insurance regulations.

In 2024 alone, there were 24 separate billion-dollar weather events – including Hurricane Helene and Hurricane Milton churning through heavily populated East Coast areas. Every catastrophic storm feeds directly back into your premium. That’s the brutal reality of how insurance pricing actually works.

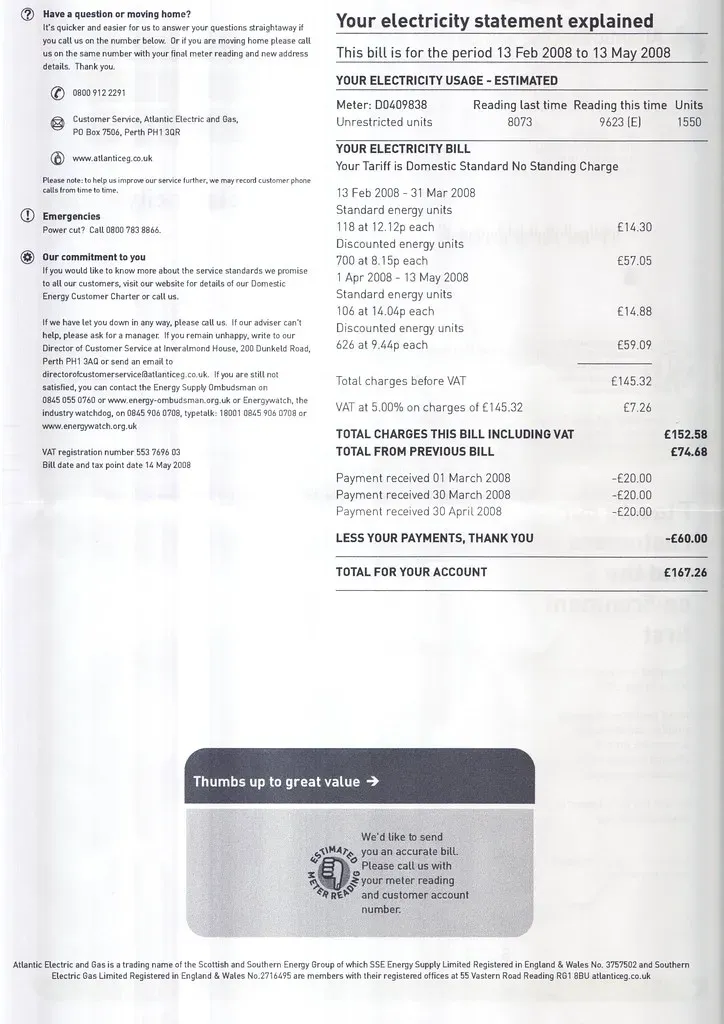

Utility Bills: The Cost of Keeping the Lights On

Electricity feels like it should just… be there. You flip a switch, things work. You don’t really think about it until the bill arrives. In 2025, prices increased for utility gas service by 10.8%, fuel oil by 7.4%, and electricity by 6.7%. These are not trivial numbers for households already stretched thin.

Electricity and natural gas – what powers your home – moved in the opposite direction from gasoline: up over 6% and nearly 14% year-over-year respectively through mid-2025, directly lifting monthly utility bills. The gas pump may feel cheaper, but your monthly utility statement tells a completely different story.

Housing, including energy costs, consumed about a third of total household spending in 2023, and because shelter and utility inflation filters through slowly, it can keep pressure on budgets even as headline inflation eases. Think of it like a slow leak in a tire. You don’t notice it immediately, but over time, you’re suddenly flat.

Shrinkflation: Paying More for Less, Without Realizing It

This one might be the sneakiest of all. I think shrinkflation is actually more psychologically damaging than a straightforward price hike – because it’s designed to fly under the radar. Shrinkflation occurs when companies reduce the size of a product in response to rising production costs. The price tag stays the same. Your product just quietly gets smaller.

On average, the per-unit price increase among downsized products ranged from 12% for paper towels to 32% for coffee. Thirty-two percent more for your morning coffee, and most people never even noticed the package shrunk. Roughly three-quarters of Americans have noticed shrinkflation at their grocery store, and of those, nearly half have abandoned a brand because of it.

The cumulative effect of multiple shrinkflation instances across a shopping cart compounds the impact on household budgets – a typical family purchasing 20 affected products monthly may receive 8 to 12% less product volume for the same expenditure compared to 2024 purchases. That’s a meaningful hit. And it doesn’t show up in any headline inflation figure.

In the U.S., roughly four in five consumers say they’re concerned about shrinkflation, up from about 73% in 2023 per YouGov data. The awareness is there. What’s harder to fight is the habit – most shoppers still reach for the same product anyway, because changing behavior takes deliberate, ongoing effort that busy lives rarely allow.

The Bigger Picture: What It All Adds Up To

Look at these five categories together and a clear pattern emerges. Groceries cost dramatically more than they did in 2020. Your streaming services have nearly doubled in some cases. Auto insurance has climbed steeply for years. Utility bills keep rising. Your packages are shrinking without your permission. None of these is officially called a tax – but the cumulative drain on your household budget is real and measurable.

Consumer sentiment remains near historic lows based on monthly University of Michigan surveys, and the cost of living still feels like it’s rising for households now paying far more for food, electricity, and housing than they were several years before inflation spiked. The numbers behind that feeling are, it turns out, very real.

The “invisible tax” is invisible precisely because it hides in plain sight. It hides in a smaller chip bag, a higher streaming tier, a quietly revised insurance premium. No ballot measure. No public debate. Just a slow, steady drain. The best defense, honestly, is simply knowing it exists – and checking your unit prices, your renewal notices, and your subscriptions more carefully than you used to. What would you have guessed was eating most of your budget? Tell us in the comments.