If you’re a high-earning professional in Las Vegas, whether you’re running a casino operation, leading a hospitality brand, managing a medical practice, owning a business, or closing real estate deals, retirement planning just got more specific in 2026. The rules around catch-up contributions have changed, and the details matter.

What Catch-Up Contributions Actually Are

Catch-up contributions allow employees aged 50 or older to make additional retirement savings above the standard annual IRS limit, designed to help older workers boost their savings in the final stretch of their careers. They’ve long been a valuable tool for high-income professionals who want to accelerate what goes into their workplace retirement plans.

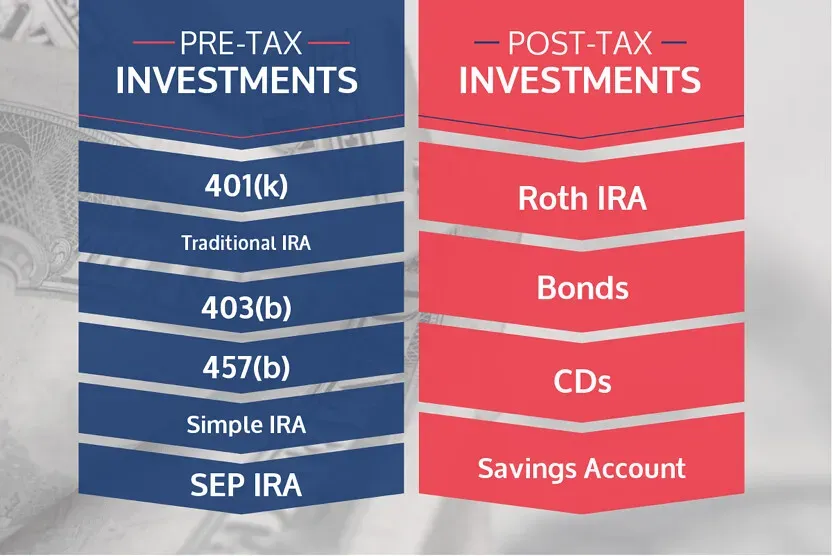

For 2026, the standard deferral limit is $24,500, and the catch-up limit for employees aged 50 and older is $8,000. That means catch-up eligible participants can contribute up to $32,500 in salary deferrals to their 401(k) plan in 2026.

The New Roth Catch-Up Rule for High Earners

Due to a provision of SECURE 2.0, high-income earners who make more than $150,000 in wages from the prior year are required to make their catch-up contributions as Roth, meaning after-tax, beginning on January 1, 2026. This is the core change that affects a significant number of Las Vegas professionals.

SECURE 2.0 changes that for the catch-up portion only, and only for one population: high earners. The standard contribution up to the base limit is not affected. Only the catch-up dollars above that base limit are subject to the new Roth requirement.

Who the Rule Actually Applies To

Beginning January 1, 2026, regular and super catch-up contributions for certain high-paid participants need to be made on an after-tax Roth basis instead of pre-tax. This rule applies to participants who have FICA wages that exceed $150,000 in the previous calendar year from the employer sponsoring the plan.

The $150,000 test looks only at wages from the current employer; wages from other employers are not combined. This is a nuance that matters for Las Vegas professionals who have multiple income streams. Participants who don’t receive FICA wages, such as partners and sole proprietors who only have self-employment income, aren’t subject to the rule.

This Does Not Eliminate Catch-Up Contributions

It’s worth saying plainly: this rule does not take catch-up contributions away. For 2026, if you’re a high-earner age 50 or older, you can choose to make pre-tax and/or Roth contributions to your retirement account up to the $24,500 limit; however, any catch-up contributions must be made to a Roth account.

If you’re 50 or older and your FICA-taxable earnings are $150,000 or more, any catch-up contributions to your 401(k) will have to be made to a Roth 401(k) with after-tax dollars. That means you’ll lose out on the upfront tax deduction you may have had previously, but you can potentially benefit from the advantages Roths can offer, including tax-free earnings and withdrawals, as long as you meet the 5-year aging rule for the plan.

The Super Catch-Up for Ages 60 Through 63

Under a change made in SECURE 2.0, a higher catch-up contribution limit applies for employees who turn 60, 61, 62, and 63 in a calendar year starting in 2025 and who participate in most 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan. For 2026, this higher catch-up contribution limit is $11,250 instead of $8,000.

For 2026, the standard limit is $24,500 and the regular catch-up adds another $8,000, for a combined ceiling of $32,500. Workers in the four-year window of ages 60 through 63 can make a super catch-up of up to $11,250, lifting their personal cap to $35,750. That’s a meaningful difference if you’re in that age window and still earning aggressively.

Once participants turn 64, they revert to the standard age 50+ catch-up contribution limit. So this higher window is time-limited, and it pays to use it while it applies. It’s also important to note that this change is optional for employers, so each plan sponsor will decide whether to implement this feature in their retirement plans.

How SIMPLE Plan Participants Are Affected

A SIMPLE IRA or a SIMPLE 401(k) plan may permit annual catch-up contributions up to $4,000 in 2026. SIMPLE plans also have their own version of the super catch-up provision under SECURE 2.0. Under a change made in SECURE 2.0, a higher catch-up contribution limit applies for employees who turn 60, 61, 62 and 63 in a calendar year starting in 2025 and who participate in SIMPLE plans. For 2026, this higher catch-up contribution limit is $5,250 instead of $4,000.

For SIMPLE plans, the final regulations clarify that the age 60 to 63 super catch-up limit and the 10 percent increase to the standard catch-up limit cannot be combined for the same participant in the same year. A SIMPLE plan may choose to offer the higher of the two limits but not both simultaneously. Small business owners in Las Vegas who sponsor SIMPLE plans should review their plan design with this in mind.

What Happens If Your Plan Doesn’t Offer Roth

If your plan does not offer a Roth 401(k) option, you won’t be able to make catch-up contributions. This is a real risk that could affect high earners in smaller Las Vegas businesses or professional practices where the plan hasn’t been updated. Starting in 2026, 401(k) plans must offer Roth contributions for high earners to make catch-up contributions at all. Because business owners often fall into this high earner group, failing to add a Roth feature could unintentionally eliminate their own ability to make catch-ups.

While plans are not required to offer Roth contributions, those that don’t will be prohibited from accepting catch-up contributions from otherwise eligible employees. This provision appears to effectively force sponsors of plans that currently allow only pre-tax catch-up contributions to either amend their plans to permit Roth deferrals, or limit catch-up eligibility to non-highly compensated employees. That’s a planning gap worth closing now.

Practical Steps Las Vegas High Earners Should Consider

The rule change is permanent, and it is also based on the prior year W-2 from the employer sponsoring the plan, which means if you earned $150,000 or more for tax year 2025, the change applies to you for the 2026 tax year. That makes the timing review straightforward: look at your 2025 wages from your employer and plan accordingly.

Participants who assume Roth treatment begins only after reaching the pre-tax limit may be surprised when reviewing pay stubs or tax forms. Checking your payroll elections now, rather than discovering the issue mid-year, avoids unnecessary confusion. Contributions for high earners will be taxed up front but can grow and be withdrawn tax-free if Roth rules are met.

Qualified Roth withdrawals don’t trigger Medicare IRMAA surcharges or push provisional income above thresholds for taxing Social Security benefits. For many high earners, that long-term benefit may outweigh the loss of the upfront deduction, but that comparison depends on your specific situation and income trajectory.

The bottom line is that the SECURE 2.0 changes to catch-up contributions are real, permanent, and in effect now. The rules don’t punish high earners; they redirect them. Knowing the thresholds, confirming your plan has Roth features, and reviewing contribution elections before the end of 2026 are practical, immediate steps worth taking. As with any retirement or tax planning decision, speak with a qualified tax or financial professional before making changes to your contribution strategy.